“Our Dollar, But Your Problem” - Global Earnings Recession Straight Ahead

The dollar’s recent rally over the last month is triggering a problem for investors globally.

It reminds me of that old saying from the Nixon Administration years, “it’s our dollar – but your problem.”

So, what exactly’s going on?

The stronger dollar is now a threat to global earnings growth. . .

Two weeks ago, I published an article highlighting the ‘not-so-great’ data that the mainstream was ignoring.

But the most important of them was the South Korean Export Growth Indicator (what I call SKEG) and its accurate history of forecasting global earnings. . .

This indicator in early May turned negative – signaling an upcoming global earnings recession. Yet at the time, the mainstream completely ignored this - if they even followed this indicator in the first place.

Since then, the market hasn’t priced in any potential risk to earnings - they’ve actually become more bullish on their earnings estimates.

This is important because a stronger U.S. Dollar and rising interest rates wreak havoc on emerging markets and foreign debtors that borrowed in dollars.

Just look at Turkey and Argentina lately. . .

This is what happens when the U.S. Dollar is the predominate global currency. If the Dollar strengthens, then foreign currencies must therefore weaken.

That’s the downside of free-floating exchange rates - if one currency goes up, then another somewhere else went down.

It makes sense why countries like Turkey are tired of being held at the dollar’s mercy. The stronger the dollar becomes, the weaker their currency – the Lira – gets.

A stronger dollar and rising rates are damaging to global earnings for two obvious reasons. . .

First, Higher rates mean higher borrowing costs.

After years of such low-rates, many forget what the ‘I’ stands for in the now-favorite valuation metric EBITDA (earnings before interest, taxes, depreciation, amortization) . . .

Yes, interest.

If interest payments rise, that translates into less earnings.

And in a world where companies are indebted up to their necks – small interest increases can be devastating to their bottom lines.

Second, a stronger dollar means foreign debtors need to convert their local currency into dollars to pay back any interest and debt owed. So, for example, if the dollar has risen 5% against their currency, they must pay 5% more.

And when you get into the billions borrowed, that extra 5% is a massive amount.

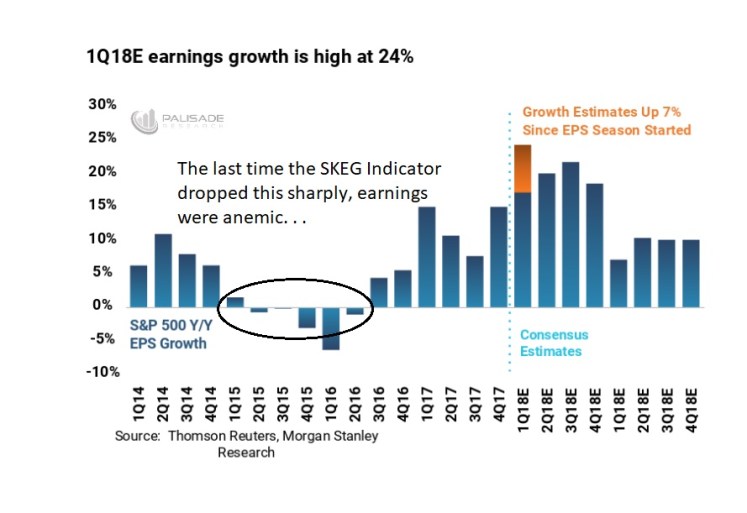

Now, looking back at the SKEG Indicator above. . .

Let’s see how earnings performed the last time South Korean Exports dropped this sharply – between the 2014 and Q4-2016 period.

Ouch - the year-over-year S&P 500 earnings growth was anemic at best. . .

Even though the last time SKEG dropped this low and global earnings soon collapsed with it – the market today doesn’t seem to care.

In fact, the crowd’s estimate for the future is very optimistic – clearly there isn’t any worry of a slowdown in global earnings.

But the SKEG Indicator is a leading-indicator – which means that it comes first. And since South Korean Export Growth has tanked, global earnings will follow.

Putting it simply - if history shows us anything, then there is a global earnings recession right up ahead.

The stronger dollar and rising rates are putting pressure on foreign economies and global corporate earnings. All it takes is one ‘less-than-stellar’ earnings report to come out and shake up Wall Street.

This will cause a sharp re-pricing of all risky assets – especially emerging markets.

I expect the mainstream to start noticing this problem sooner than later. Don’t be behind the herd on this one.

The SKEG Indicator is an important and useful leading-indicator for a reason. its accuracy of forecasting global earnings is hard to deny.

Let’s not start saying “but this time is different”. . .